Redefining the 4% Rule for 2026

Retirement Best Strategies Guide 2026, the “4% Rule” is officially a relic of a simpler era. As we navigate the mid-2020s, a decade defined by erratic inflation and higher-than-average market uncertainty, the quest for a single, static withdrawal number has proven to be a fool’s errand. Modern retirement science has shifted its focus from the “perfect math” to “perfect behavior.”

A definitive study by Morningstar has recalibrated our understanding of portfolio longevity. By analyzing a 30-year retirement horizon with a 90% success rate across consistent market simulations, researchers discovered that success isn’t governed by a fixed rate, but by how your withdrawals respond to market reality. In 2026, the most resilient retirees aren’t those with the most complex spreadsheets, but those who have adopted dynamic systems that align with their personal psychology.

Retirement Best Strategies Guide 2026

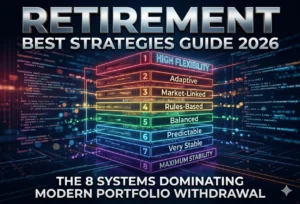

The 8 Dominant Withdrawal Frameworks for Portfolio Longevity

I. The Fixed Real Withdrawal Method (The Baseline)

This serves as the benchmark for all modern strategies. It mimics a traditional salary, providing a predictable “retirement paycheck” regardless of market swings.

- Mechanism: You establish a starting withdrawal rate (3.9% in the Morningstar model) and adjust the dollar amount annually based solely on inflation.

- The 2026 Math ($1M Portfolio): A retiree starts with $39,000 in Year 1. Assuming a 2.5% average inflation rate, the withdrawal scales to approximately $40,000 in Year 2, $49,000 in Year 10, and $63,000 by Year 20. These are “real” inflation-adjusted dollars.

Trade-offs:

- Pros: Maximum predictability; simplifies household budgeting; provides high psychological comfort during market corrections.

- Cons: Requires the lowest starting withdrawal rate (3.9%) to ensure safety; ignores portfolio growth, leading to a high risk of “underspending” and leaving significant assets on the table.

II. Skip Inflation After a Loss (The Capital Preserver)

This is a “surgical” adjustment to the baseline. It follows the Fixed Real method but introduces a minor sacrifice to protect the portfolio’s lifespan.

- Mechanism: If your portfolio experiences a negative return in the previous year, you skip your annual inflation raise. Your spending remains the same in nominal dollars but stays flat rather than increasing.

- Analysis: This “skipped raise” permanently lowers your future spending path. It provides a significant boost to portfolio durability—especially in the early years of retirement—without the trauma of a direct spending cut.

Target Profile: Retirees who want a salary-like feel but are willing to let their purchasing power lag slightly after bad years to ensure they never outlive their money.

III. The Required Minimum Distribution (RMD) Method

This strategy leverages the IRS’s own longevity math to ensure you never outlive your capital. It is mathematically impossible to hit zero using this method.

- Mechanism: You divide your year-end portfolio balance by your remaining life expectancy (using IRS divisors). As you age, the divisor shrinks, causing your withdrawal percentage to naturally increase.

- The 2026 Math ($1M Portfolio): At age 67, with a 30-year expectancy, the baseline start is $33,000 (3.3%).

- Volatility Comparison:

- Scenario A (Strong Market): If the portfolio grows to 1.15M and life expectancy drops to 29 years, the draw jumps to 39,700 (a 20% raise).

- Scenario B (Bad Market): If the portfolio falls to 850,000 and life expectancy drops to 29 years, the draw plummets to 29,300 (a sharp pay cut).

IV. The Guardrails (Guyton-Klinger) Model

Think of this as “cruise control.” It allows for higher initial spending by using “drift” triggers to keep the plan on track.

- Mechanism: You set an initial target (e.g., 4%). If market performance causes your actual withdrawal rate to “drift” 20% away from that target (either too high or too low), it triggers a 10% adjustment to your spending.

- Analysis: If a $1M portfolio grows to $1.4M, your withdrawal rate has drifted too low; the system triggers a 10% raise. If the portfolio drops to $670,000, your withdrawal rate has drifted dangerously high; it triggers a 10% cut. This is the “Middle Ground” between RMD volatility and Fixed Real rigidity.

V. The Actual Spending Decline Strategy

This strategy acknowledges the behavioral reality of aging: most retirees naturally spend less as they get older.

- Mechanism: Instead of increasing spending with inflation, this model assumes a 2% annual decline in real spending.

- The 2026 Math ($1M Portfolio):

- Year 1: $40,000

- Year 10: $32,500

- Year 20: $26,500

- The “Smile” Curve Warning: While this strategy yields a high success rate by reducing pressure on the portfolio, a Senior Strategist must note the “smile” curve. While discretionary spending drops in the middle years, healthcare costs often cause a spike in the final years of life.

VI. The Constant Percentage Withdrawal

This is the most technically efficient but emotionally taxing method. It treats your portfolio like a business partnership.

- Mechanism: You take a fixed percentage (e.g., 5%) of the current portfolio value every single year, regardless of what is happening in the world.

Volatility Shock (Initial $1M Portfolio at 5% Rate): | Market Outcome | Portfolio Value | Annual Withdrawal | | :— | :— | :— | | Strong Gain | 1.3 Million | **65,000** ($15,000 Raise) | | Significant Loss | 700,000 | **35,000** ($15,000 Cut) |

Analysis: This is only viable for retirees with a strong “Income Floor” (Social Security/Pensions) that covers all essential bills.

VII. The Endowment Method (10-Year Rolling Average)

Institutional discipline brought to the individual level. This method is used by major universities to fund operations through decades of volatility.

- Mechanism: Your annual withdrawal is a fixed percentage (e.g., 5%) based on the rolling 10-year average of your portfolio value.

- The “Lag” Benefit: This creates a significant smoothing effect. Today’s spending is influenced by a market peak (or trough) from years ago, preventing “whipsaw” lifestyle changes. On a $1M portfolio, a 5% draw based on a rolling average ensures that a single bad year in 2026 doesn’t force a drastic cut in 2027.

VIII. The Vanguard Floor and Ceiling Model

This is a refined, behaviorally-focused version of the guardrail system. Unlike Guyton-Klinger, which uses “drift” triggers, Vanguard uses absolute percentage caps.

- Mechanism: You adjust your spending for inflation, but you apply a Ceiling (e.g., +5%) and a Floor (e.g., -2.5%).

- Analysis: If the market surges, the 5% ceiling prevents “lifestyle leaps” that often lead to future regret. If the market crashes, the -2.5% floor prevents “panic-level belt-tightening.” This is widely regarded as the most realistic model for the average investor in 2026.

Retirement Best Strategies Guide 2026

Macro Analysis: The Shift in Retirement Science

The fundamental trade-off in the 2026 landscape is Spending vs. Stability. If you want to maximize the total dollars spent over your lifetime, you must accept year-to-year variability (RMD or Constant Percentage). If you want a smooth, predictable life, you must accept a lower starting rate and the risk of leaving a large unspent legacy (Fixed Real).

The deciding factor is the “Income Floor.” If Social Security and pensions cover your “must-pay” bills, you can afford to be aggressive and volatile with your portfolio. If your portfolio is your only source of bread and butter, you must prioritize “Floor-based” or “Guardrail” systems.

Retirement Best Strategies Guide 2026

Strategic Selection: The 2026 Decision Tree

- Is predictable monthly income required for your peace of mind?

- Yes: Select Fixed Real, Skip Inflation, or Actual Spending Decline.

- No: Proceed to Question 2.

- Are you comfortable adjusting your lifestyle based on market performance?

- Yes: Consider Guardrails or the Vanguard Model.

- Highly Yes: Use RMD, Constant Percentage, or Endowment methods.

- Is your primary goal to maximize spending or preserve a legacy?

- Maximize Spending: RMD or Constant Percentage (Probability-based success).

- Preserve Legacy: Fixed Real or Actual Spending Decline.

- Does your household have a strong guaranteed income floor?

- Yes: You can tolerate high volatility for higher lifetime upside.

- No: Stability and “Floor-based” models are non-negotiable.

Retirement Best Strategies Guide 2026

FAQ: Navigating Retirement Withdrawals in 2026

What is the “best” withdrawal strategy?

There is no single “best” rate. The best strategy is the one that aligns with your specific behavior, allowing you to stay disciplined during market downturns without panicking.

How can I avoid running out of money?

The RMD and Constant Percentage methods are mathematically bulletproof; because they always take a percentage of the remaining balance, the portfolio can never hit zero.

What is the risk of underspending in retirement?

The “Fixed Real” method often results in retirees leaving millions on the table because it never gives “permission” to spend more when the market performs well.

How does inflation impact these models?

Fixed Real and Vanguard models prioritize inflation protection. In contrast, RMD and Constant Percentage focus entirely on portfolio value, meaning your “real” purchasing power can fluctuate wildly.

What is the “Fixed Real” baseline?

It is the classic approach: take a set amount (starting around 3.9% of $1M) and increase that dollar amount by the inflation rate every year, regardless of market performance.

How does the “Guardrails” method work?

It acts as cruise control, triggering 10% raises when the portfolio is up significantly and 10% cuts when the withdrawal rate drifts too high relative to the portfolio value.

What is the impact of early-retirement market losses?

Early losses (Sequence of Returns Risk) can break a static plan. Dynamic models like “Skip Inflation After a Loss” are designed specifically to preserve capital during these fragile early years.

Why does spending decline as retirees age?

Data shows retirees naturally slow down—spending less on travel and discretionary items. The “Actual Spending Decline” model builds this 2% annual real reduction into the plan.

What is the difference between the Vanguard model and standard Guardrails?

Standard Guardrails (Guyton-Klinger) use “drift” triggers (how far you are from the original % target), while Vanguard uses absolute percentage caps (Floors and Ceilings) to limit annual change.

How does the Endowment method smooth out market noise?

By using a 10-year rolling average, a sudden market crash only accounts for 10% of the calculation for your next withdrawal, preventing “whipsaw” spending cuts.

Retirement Best Strategies Guide 2026

Investor Conclusion: The Psychology of Success

A “perfect plan on paper” is useless if it causes you to sell in a panic during a market correction. In 2026, the hallmark of a Senior Retirement Strategist is recognizing that retirement is 20% math and 80% behavior.

Your directive is simple: Identify your “Income Floor,” determine your tolerance for spending variability, and select a system that you can maintain emotionally. Success isn’t about beating the market—it’s about having a system that beats your own anxiety. Focus on long-term alignment, ignore the daily headlines, and let your chosen system do the heavy lifting.

Disclaimer: All investing carries risk. This report is for informational and educational purposes only and does not constitute financial advice. Past performance is not indicative of future results. Always perform individual research or consult with a qualified financial advisor before making investment decisions.